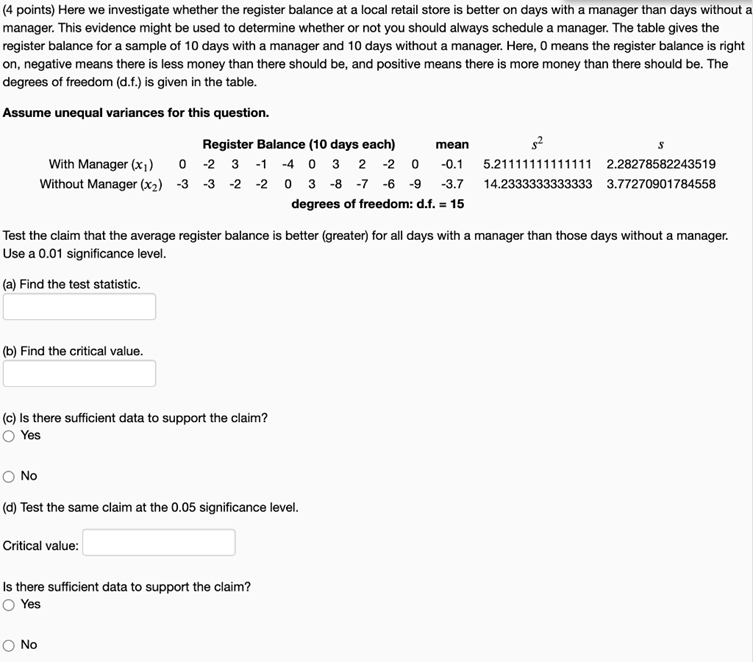

Here we investigate whether the register balance at a local retail store is better on days with a manager than days without a manager. This evidence might be used to determine whether or not you should always schedule a manager. The table gives the register balance for a sample of 10 days with a manager and 10 days without a manager. Here, O means the register balance is right on, negative means there is less money than there should be, and positive means there is more money than there should be. The degrees of freedom (d.f.) is given in the table. Assume unequal variances for this question. 52 S With Manager (x1) 0 Without Manager (x2) -3 Register Balance (10 days each) mean -2 3 -1 -4 0 3 2 -2 0 -0.1 -3 -2 -2 0 3 -8 -7 -6 -9 -3.7 degrees of freedom: d.f. = 15 5.21111111111111 14.2333333333333 2.28278582243519 3.77270901784558 Test the claim that the average register balance is better (greater) for all days with a manager than those days without a manager. Use a 0.01 significance level. (a) Find the test statistic. (b) Find the critical value. (c) Is there sufficient data to support the claim? O Yes O No (d) Test the same claim at the 0.05 significance level. Critical value: Is there sufficient data to support the claim? O Yes Ο Νο

#Sales Offer!| Get upto 25% Off: