Comprehensive Stockholders’ Equity Transactions

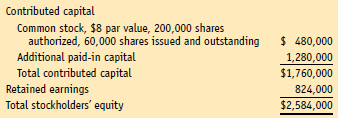

On December 31, 20×7, the stockholders’ equity section of Tsang Company’s balance sheet appeared as follows:

The following are selected transactions involving stockholders’ equity in 20×8: On January 4, the board of directors obtained authorization for 20,000 shares of $40 par value noncumulative preferred stock that carried an indicated dividend rate of $4 per share and was callable at $42 per share. On January 14, the company sold 12,000 shares of the preferred stock at $40 per share and issued another 2,000 in exchange for a building valued at $80,000. On March 8, the board of directors declared a 2-for-1 stock split on the common stock. On April 20, after the stock split, the company purchased 3,000 shares of common stock for the treasury at an average price of $12 per share; 1,000 of these shares subsequently were sold on May 4 at an average price of $16 per share. On July 15, the board of directors declared a cash dividend of $4 per share on the preferred stock and $.40 per share on the common stock. The date of record was July 25. The dividends were paid on August 15. The board of directors declared a 15 per- cent stock dividend on November 28, when the common stock was selling for $20. The date of record for the stock dividend was December 15, and the dividend was to be distributed on January 5.

Required

1. Record the above transactions in journal form.

2. Prepare the stockholders’ equity section of the company’s balance sheet as of December 31, 20×8. Net loss for 20×8 was $218,000. (Hint: Use T accounts to keep track of transactions.)

3. User Insight: Compute the book value per share for preferred and common stock (including common stock distributable) on December 31, 20×7 and 20×8, using end-of-year shares outstanding. What effect would you expect the change in book value to have on the market price per share of the company’s stock?